Happy New (Taxation) Year

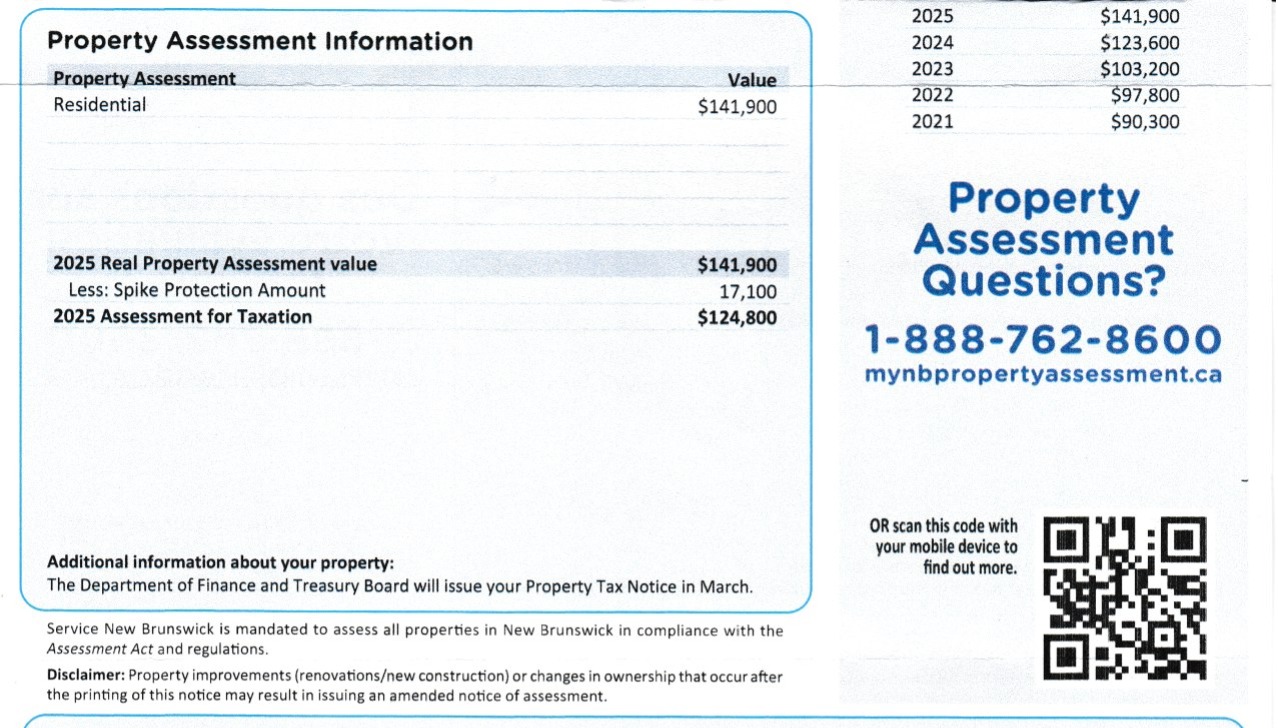

On your recently-received 2025 Property Assessment Notice, which Service New Brunswick (SNB) sent you, you’ll note the two values in the section entitled, “Property Assessment Information”.

Want to understand our property assessment and taxation system better and make it work to your advantage?

See my new book:

Taxing New Brunswick: An Insider’s Guide to Successfully Challenging Your NB Property Assessment (available on Amazon)

One is the “Real Property Assessment value” and the other is your “Assessment for Taxation”. Your tax will be based on the “Assessment for Taxation” value (note that Finance and Treasury Board [FTB] issues tax notices on March 1) and it’s created when SNB subtracts the “Spike Protection Mechanism” (SPM) from the “Real Property Assessment value”.

For example, our own 2025 “Real Property Assessment value” is $141,900. However, our “Assessment for Taxation” is only $124,800, which represents a 10% increase from what the “Assessment for Taxation” was last year. FTB will therefore tax us on the $124,800, not the $141,900.

(Note: don’t worry about how they do the calculations for the SPM – just make sure your 2025 “Assessment for Taxation” is no more than 10% higher than last year’s.)

What is the ‘Spike Protection Mechanism’ (SPM)?

As per Service New Brunswick’s information on last year’s Property Assessment Notice itself, “Spike Protection prevents your Assessment for Taxation from increasing more than 10% a year (excluding new construction, properties sold in the previous year, or major improvements)”.

At first glance, you might think that using the SPM to limit tax increases in a given year would be a good idea because, you know, less tax.

But is it? Well, the part about limiting tax increases in a given year is indeed a good thing, I’d argue. But using the SPM to do that? Not so much.

In fact, I think that the SPM is as monumentally stupid and counterproductive a piece of public policy as there is in NB. And there are several reasons for that.

Reason #1: SPM spreads out tax increases but does not reduce the tax burden

The first reason is that the SPM limits the amount of increase in taxes you might expect in a given year but doesn’t limit the tax burden overall. The SPM spreads the increase out over more than one year but doesn’t eliminate the overall increase itself.

As a result, your municipality (and the Province, if your property is also subject to Provincial tax) can expect to receive additional tax revenue every year whether their budget calls for it or not.

What happens, then, is that the municipality tends to tailor its budget to the expected revenue rather than doing it correctly, which is to requisition only the revenue needed and set their tax rate according to those budgetary needs. Not that municipalities don’t need more sustainable and diverse funding, but this isn’t the right way to get that additional revenue.

Reason #2: SPM creates inequities in the system

You’ll note from the SNB definition above that SPM doesn’t apply to new construction or properties with major improvements (or vacant land). What it doesn’t mention is that the SPM is also re-set when the property changes hands.

So if we take our own situation as an example again, the 10% SPM limit on the “Assessment for Taxation” means that we will see at least a 10% increase in property tax for 2025 (and more if they raise the tax rate in the rural areas of Kent County). Last year’s tax was $1,287; this year’s will be at least $1,416.

But what if we’d sold our house last year? In that case, the new owners would be looking at paying property tax based on the full value of $141,900, which equals $1,609 (assuming no change in tax rates) – a 25% increase. That’s an additional $322. What if our “Real Property Assessment value” were $250K and/or subject to Provincial tax because it’s a second property? Or, worse yet, an apartment? How many additional dollars would that be?

And worse yet, the problem compounds every year to the advantage of those who stay in a single home for an extended period. As a result, people will look at property tax values on SNB’s Property Assessment On Line and see widely divergent tax amounts for what are often very similar properties.

Why does the system subsidize long-term ownership this way and how exactly does this inequity serve the public good?

Reason #3: SPM is the wrong tool for the job

You wouldn’t use plumbing tools to fix an electrical problem, so why is NB using an assessment tool, namely SPM, to fix what is a tax problem? Nothing bad could possibly come from that, could it?

Some readers may remember California’s Proposition 13 in 1978. It’s not exactly like SPM but it was (and is) still an assessment tool being used to fix what people perceived to be a tax problem then. This is what a report from the US National Bureau of Economic Research had to say about Proposition 13:

As a consequence of Proposition 13, homeowners in California receive a property subsidy that increases the longer that they own their home. It has been described as a contributor to California’s housing crisis, as its acquisition value system (where the assessed value of property is based on the date of its acquisition rather than current market value) incentivizes long-time homeowners to hold onto their properties rather than downsize, reducing the housing supply and raising housing prices.

Other taxing jurisdictions have also tried assessment solutions similar to SPM as a way of addressing tax issues. I’m not specifically conversant with any of these but I do know that limiting assessments places ratepayer focus on assessments and assessors instead of on the politicians who actually set the tax rates, be they provincial or municipal. That’s unconscionable.

Assessments are not tax-generation or tax-suppression tools; they are tools to determine relative ability to pay, period. Problems abound when governments employ them otherwise.

So what’s the solution?

The solution is actually very simple: start by eliminating the stupid assessment-based SPM as a way of keeping a lid on tax increases. Start using actual tax solutions to address what is fundamentally a tax problem.

Adjust the tax rates so they are revenue neutral, i.e., where taxes don’t increase just because assessments do (columns on both tax rates and revenue neutrality are forthcoming).

In conjunction with that, have the taxing authority, whether it be the municipality, the Province, or both, requisition property tax funding on the basis of budgetary need rather than tailoring the budget to how much additional tax revenue is expected and then cutting the tax rate just a bit to show how much taxing authorities really care about those poor, beleaguered ratepayers.

Finally, apply the same property solution to every property, regardless of when owners built, when they purchased, or whether the assessment increased because of “major improvements”.

That’s it. Let Service New Brunswick focus on assessments, while Finance and Treasury Board focusses on taxes. Never the twain should meet.

People might then start (and only start) seeing the system as a bit fairer, rather than as the broken, archaic, and non-transparent mess that it is.

This piece was first published in the Northumberland Free Press, 2025-01-25

Excerpt from TAXING NEW BRUNSWICK

Other articles on assessment & taxation

(most recent article first)

Battle aborted: Shutting down the TAXING NB project

Holt gets passing grade for property assessment freeze – for now

Residential vs. Non-residential tax rates: The forced link between the two is costing you money

Tax agents: Battling those big, bad assessors on behalf of the little guy?

With no revenue neutrality, NB “fails to meet the test of open and transparent property taxation”

Municipal budgets: About those ‘tax rate cuts”…

Your Property Assessment Notice is here – now what?

New property assessment valuation date in 2025 – how does this affect you?

Property assessment and taxation reform: the Real Property Tax Act

Why “lowered tax rate” isn’t the right headline

Property assessment and taxation reform: the Assessment Act

Property assessment and taxation reform: backgrounder

Malign design: Nine ways to build a broken property tax system

Hi Jerry, your article resonates well for those in Nova Scotia who deal with the Cap Assessment Program. Since 2005, it’s created an administrative burden for government staff, home owners believe it’s unfair and not transparent. Some municipalities wish to scrap this cap! There are many unintended consequences such as an incentive to create family trusts to ensure peoples eligibility remains which is more favourable to those highest valued luxury residences as opposed to those struggling to pay their taxes. The barriers to entry remain high for those living in areas where assessment remain out of date and distorted by difficult to understand fundamentals based on eligibility as opposed to market based principles.

https://www.nsfm.ca/images/Resolution_1_-_CAP.pdf

Click on the link in the comment above, as it sums up the problems with assessment caps in general and the consequences of the assessment cap in Nova Scotia in particular. Quote from that paper:

“While the CAP is a provincial program, municipalities are being asked by more and

more residents why they pay more property taxes than their neighbour. New home

buyers, whether first time buyers or seniors looking to downsize, are faced with higher

property taxes than neighbouring homes, even though services are the same.

NSFM has known since 2007 that the CAP had shifted the tax burden from

homeowners with capped properties to those with uncapped properties.”

Great piece by CBC’s Robert Jones on the stupidity of the SPM: https://www.cbc.ca/news/canada/new-brunswick/young-new-brunswick-homeowners-paying-highest-property-taxes-1.7443100

Dovetails perfectly with my piece above, as it turns out.

The piece includes this quote about SPM from a government representative: “However, Mark Taylor, a spokesperson for the government, defended how the policy works and said in a statement that ‘the objective’ of spike protection is to ‘maintain stability for existing property owners,’ not to be concerned about whether new homeowners are being made to pay hundreds of dollars more in property tax than neighbours.’

‘Buyers are, or should be, aware when they are buying a property that they are paying market value,’ Taylor’s statement said.”

And that’s why I had to quit working for the government – because it puts you in the position of occasionally having to defend the stupid and sounding typically oblivious in the process. No wonder people want to scream.