The dreaded envelope

In that the third week of January is when our property assessment notices arrive, it’s a time of year that fills many New Brunswickers with dread.

Want to understand our property assessment and taxation system better and make it work to your advantage?

See my new book:

Taxing New Brunswick: An Insider’s Guide to Successfully Challenging Your NB Property Assessment (available on Amazon)

Why? With this archaic and very broken property tax system we have here, it’s because increased assessments appear to lead to increased taxes (they actually don’t – it’s the government budgets that do that). It’s not like that in most Canadian taxing jurisdictions but it is here, so we tremble when we open that envelope from Service New Brunswick.

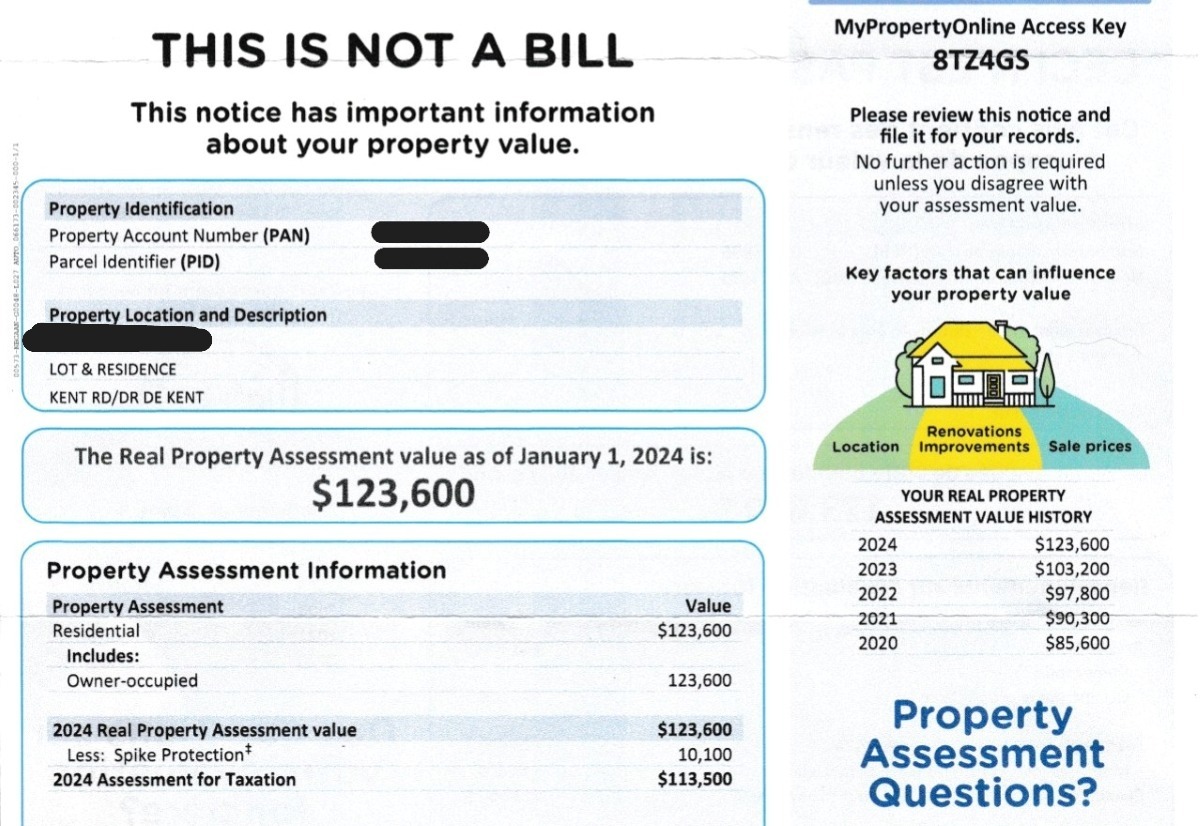

Your assessment notice may read, “This is not a bill,” but you’re all too well aware that you’ll be paying the piper soon enough (March 3, to be exact).

Regardless of your level of fear in seeing your name in that envelope’s window, there are a couple of things critical to understanding your assessment notice in general and this year’s notice in particular.

A new valuation date

The first thing to know is that there is a new valuation date in play for 2025.

Starting this year, your assessed value will be based on January 1 of the previous year – 2024, in this case – instead of the current year. This means that your assessment will be based on market activity, not during the past year (2024), as was the case up to this point, but during the year before that (i.e., throughout 2023).

This is actually very sound practice and brings that part of NB’s property tax system in line with what other Canadian assessment jurisdictions are doing. However, this doesn’t mean that your 2025 “Real Property Assessment value” (as it’s called on the notice) will be exactly the same as last year’s (for reasons I won’t go into here); in fact, it’s likely to be a lot more.

“Real Property Assessment value” vs. “Assessment for Taxation”

However, your assessment notice may have two values: one is the “Real Property Assessment value” and the other is your “Assessment for Taxation”, which are two very different things. Or at least they might be, depending on how much your property’s assessed value has increased over the past couple of years.

Both values are important but for different reasons.

The “Real Property Assessment value” (i.e., what assessment legislation calls the “Real and True Value”) is what the assessor thinks your property is actually worth, so this is important because it’s the value that you will be challenging if you choose to submit a Request for Assessment Review (RFR).

On the other hand, the “Assessment for Taxation” is important because it’s exactly what it sounds like – it’s the amount that determines how much tax you actually pay. This comes into play if your property is subject to what’s known as the “Spike Protection Mechanism” (SPM), which ensures that your “Assessment for Taxation” cannot be more than 10% higher than it was last year (I’ll talk more about the SPM and why it is bad public policy in a future column).

Note that the SPM is not relevant if the increase in your “Real Property Assessment value” is less than 10%. In that case, your “Real Property Assessment value” and your “Assessment for Taxation” will be the same and you will pay tax based on that amount.

What if you disagree with your assessment?

Property owners have the right to challenge their assessments. The first step in this process is submitting a Request for Assessment Review (RFR), the details of which appear on your notice (pay particular attention to the deadline date).

But should you challenge your assessment? The answer is a firm “maybe”. There are really only two main reasons to submit an RFR:

- you are absolutely certain that your property would have sold for less than the assessed value on the January 1, 2024, valuation date; or

- you believe that the assessor is unaware of some type of physical, functional, or external depreciation pertaining to your property – this is especially so if you are certain that there has not been an assessment inspection for many years.

That’s it. Notwithstanding some possible exceptions, those are the only reasons, so let’s assume you’ve decided to challenge.

What to avoid in requesting an assessment review

Upon submitting an RFR, there is a section asking you your reasons. In my 3.5 years as an assessor, I saw every possible reason for RFRs – some funny, some irrelevant, some ignorant (as in genuinely not understanding the system), and some downright offensive.

Remember that an RFR is about reviewing the value of your property as of the valuation date and nothing else. It’s not about:

- your taxes – you can’t challenge just because you think your taxes are too high;

- your neighbourhood services, unless your own property’s services are substandard to those around you;

- the amount of any increase -if you get a big increase in one year, it’s likely you were underassessed for several years prior, so no complaining allowed – it’s not a basis for an assessment reduction anyway;

- assessment equity – based on current assessment legislation, you can’t submit an RFR on your property because it’s assessed for more than the exact same property next door – yes, this sucks, but that’s our system at this point;

- how the government is screwing you over;

- calling assessor’s intelligence, competence, or integrity into question; and

- claiming that your property is somehow worth less than what you just paid for it, unless you have a very good reason.

So by all means submit an RFR but word it so that it maximizes your chances of success. On the other hand, don’t waste your and the assessor’s time if your property really would sell for the assessed value or more.

Forewarned is forearmed

Knowing all these things in advance will perhaps lessen the strain of opening that assessment notice envelope when it arrives. At least you’ll now understand the notice better and know what your options are after that.

And remember that the assessment notice is only the first shoe to drop – the other drops when Finance and Treasury Board (not Service New Brunswick) sends you your tax notice at the beginning of March.

Broken as it is, it’s the system we have in place right now. Do everything you can to understand it and make it work in your favour.

This piece was first published in the Northumberland Free Press, 2025-01-18

Excerpt from TAXING NEW BRUNSWICK

Other articles on assessment & taxation

(most recent article first)

Battle aborted: Shutting down the TAXING NB project

Holt gets passing grade for property assessment freeze – for now

Residential vs. Non-residential tax rates: The forced link between the two is costing you money

Tax agents: Battling those big, bad assessors on behalf of the little guy?

With no revenue neutrality, NB “fails to meet the test of open and transparent property taxation”

Municipal budgets: About those ‘tax rate cuts”…

The ‘Spike Protection Mechanism (SPM) does property owners no big favour

New property assessment valuation date in 2025 – how does this affect you?

Property assessment and taxation reform: the Real Property Tax Act

Why “lowered tax rate” isn’t the right headline

Property assessment and taxation reform: the Assessment Act

Property assessment and taxation reform: backgrounder

Malign design: Nine ways to build a broken property tax system